- Professional Development

- Medicine & Nursing

- Arts & Crafts

- Health & Wellbeing

- Personal Development

220 Courses in Manchester

Board Meeting Prep - Tips and Tools

By Ralph Ward

Board members face a huge amount of information and review before the board meeting. Here is step-by-step process for mastering your board meeting prep challenge.

Overview This two-day intensive course is ideal for finance professionals seeking to deepen their expertise in options trading and volatility management. The course will cover option pricing and risk management techniques. Exploring differences between physical and cash-settled options European versus American/Bermudan options, and the implications of deferred premiums. Examining the role of volatility in option pricing & Managing First-Generation Exotics. Who the course is for Derivative traders Quants and research analysts Fund managers, fund of funds Structured product teams Financial and valuation controllers Risk managers and regulators Bank and corporate treasury managers IT Course Content To learn more about the day by day course content please click here To learn more about schedule, pricing & delivery options, book a meeting with a course specialist now

Making the Case: Building a Strong Business Case for EV Infrastructure

By Cenex (Centre of Excellence for Low Carbon & Fuel Cell Technologies)

Need to justify EV infrastructure? This workshop shows you how to build a strong, clear business case that wins support and funding.

BESPOKE FUTURE TRANSPORT WORKSHOPS: Tailored to meet your needs

By Cenex (Centre of Excellence for Low Carbon & Fuel Cell Technologies)

Need EV training that fits your goals? Our bespoke workshops are built around your challenges—designed with you, for you.

Power Play: How the Energy System Really Works (and Why It Matters)

By Cenex (Centre of Excellence for Low Carbon & Fuel Cell Technologies)

How does the energy system work and what does it mean for EVs? This interactive session puts your team in charge of the grid. Game on.

Cyclum Vitae: Using Life Cycle Analysis to Explore the True Impact of EVs & Infrastructure

By Cenex (Centre of Excellence for Low Carbon & Fuel Cell Technologies)

What’s the real impact of EVs and infrastructure? This hands-on session uses gameplay to explore life cycle trade-offs and build shared understanding.

INTERNATIONAL CUSTOMS

By Export Unlocked Limited

This module aims to develop knowledge and understanding of customs procedures associated with international trade. The module includes trade agreements, tariffs and taxes, immigration, intellectual property rights, clearance procedures, transport regulations, sanitary and Phyto-sanitary measures, customs valuation, preference systems and anti-dumping measures.

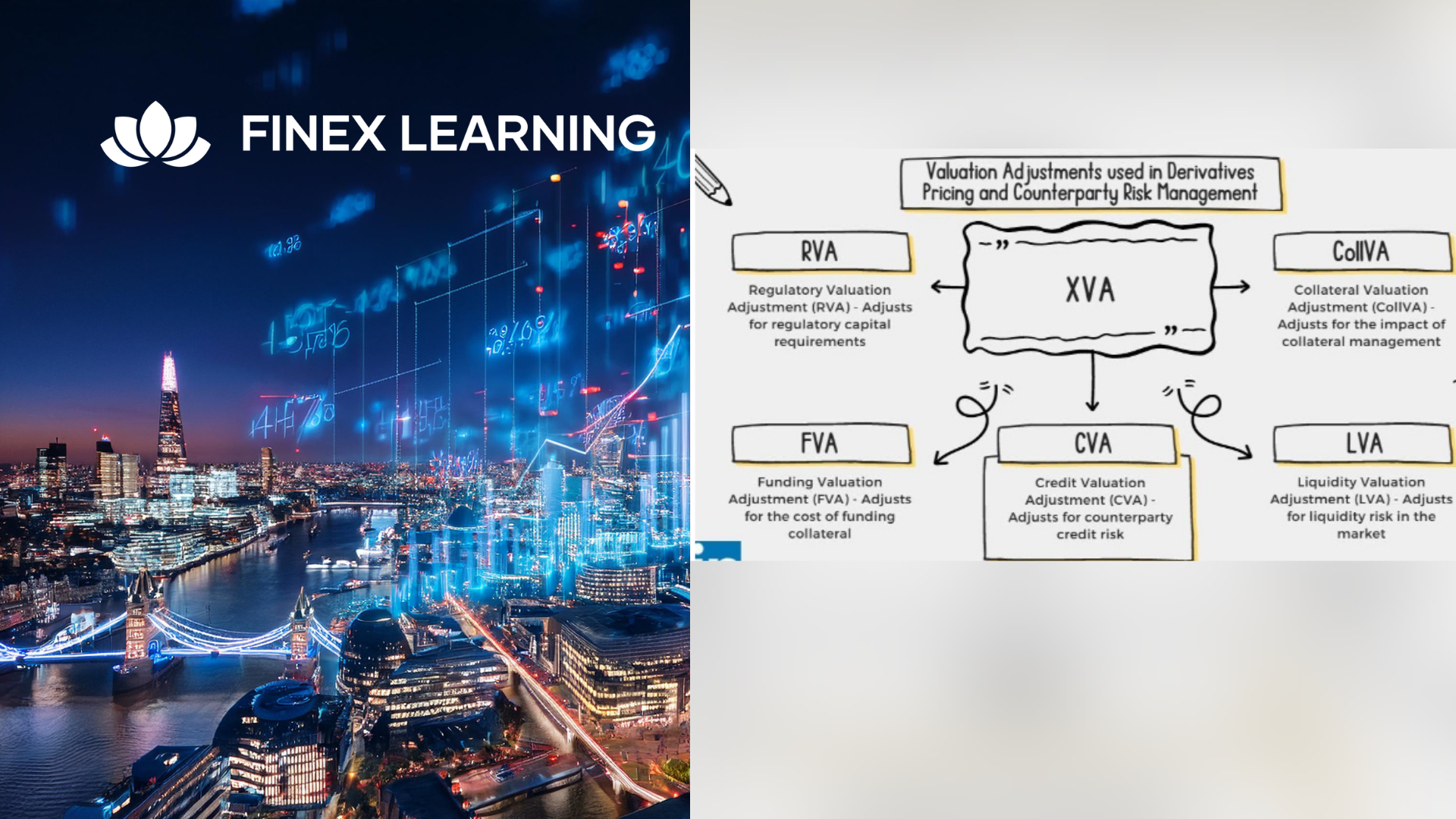

Overview This is a 2 day course on understanding credit markets converting credit derivatives, from plain vanilla credit default swaps through to structured credit derivatives involving correlation products such as nth to default baskets, index tranches, synthetic collateralized debt obligations and more. Gain insights into the corporate credit market dynamics, including the role of ratings agencies and the ratings process. Delve into the credit triangle, relating credit spreads to default probability (PD), exposure (EAD), and expected recovery (LGD). Learn about CDS indices (iTRAXX and CDX), their mechanics, sub-indices, tranching, correlation, and the motivation for tranched products. The course also includes counterparty risk in derivatives market where you learn how to managed and price Counterparty Credit Risk using real-world, practical examples Understand key definitions of exposure, including Mark-to-Market (MTM), Expected Exposure (EE), Expected Positive Exposure (EPE), Potential Future Exposure (PFE), Exposure at Default (EAD), and Expected Loss (EL) Explore the role of collateral and netting in managing counterparty risk, including the key features and mechanics of the Credit Support Annex (CSA) Briefly touch upon other XVA adjustments, including Margin Valuation Adjustment (MVA), Capital Valuation Adjustment (KVA), and Collateral Valuation Adjustment (CollVA). Who the course is for Credit traders and salespeople Structurers Asset managers ALM and treasury (Banks and Insurance Companies) Loan portfolio managers Product control, finance and internal audit Risk managers Risk controllers xVA desk IT Regulatory capital and reporting Course Content To learn more about the day by day course content please click here To learn more about schedule, pricing & delivery options, book a meeting with a course specialist now

Overview 1 day course on IFRS 9 expected credit loss modelling, both for financial statement and capital stress testing purposes Who the course is for Credit risk management Quants ALM staff Finance Internal audit External auditors Bank investors – equity and credit investors Course Content To learn more about the day by day course content please click here To learn more about schedule, pricing & delivery options, book a meeting with a course specialist now

Overview This is a 2 day applied course on XVA for anyone interested in going beyond merely a conceptual understanding of XVA and wants practical examples of Monte Carlo simulation of market risk factors to create exposure distributions and profiles for derivatives used for XVA pricing Learn how to do Monte Carlo simulation of key market risk factors across major asset classes to create exposure distributions and profiles (with and without collateral) for derivatives used for XVA pricing. Learn how to calculate each XVA. Learn sensitivities of each XVA and how XVA desks manage these. Learn regulatory capital treatment of counterparty credit risk (both for CCR and CVA volatility) and how to stress test this within ICAAP or system-wide external, supervisor-led capital stress test. Who the course is for Anyone involved in OTC derivatives XVA traders XVA quants Derivatives traders and salespeople Risk management Treasury staff Internal audit and finance Course Content To learn more about the day by day course content please click here To learn more about schedule, pricing & delivery options, book a meeting with a course specialist now