Booking options

Price on Enquiry

Price on Enquiry

Delivered Online or In-Person

Delivered at your location

UK & International Requests Considered

Two days

All levels

Overview

This is a 2 day applied course on XVA for anyone interested in going beyond merely a conceptual understanding of XVA and wants practical examples of Monte Carlo simulation of market risk factors to create exposure distributions and profiles for derivatives used for XVA pricing

Learn how to do Monte Carlo simulation of key market risk factors across major asset classes to create exposure distributions and profiles (with and without collateral) for derivatives used for XVA pricing.

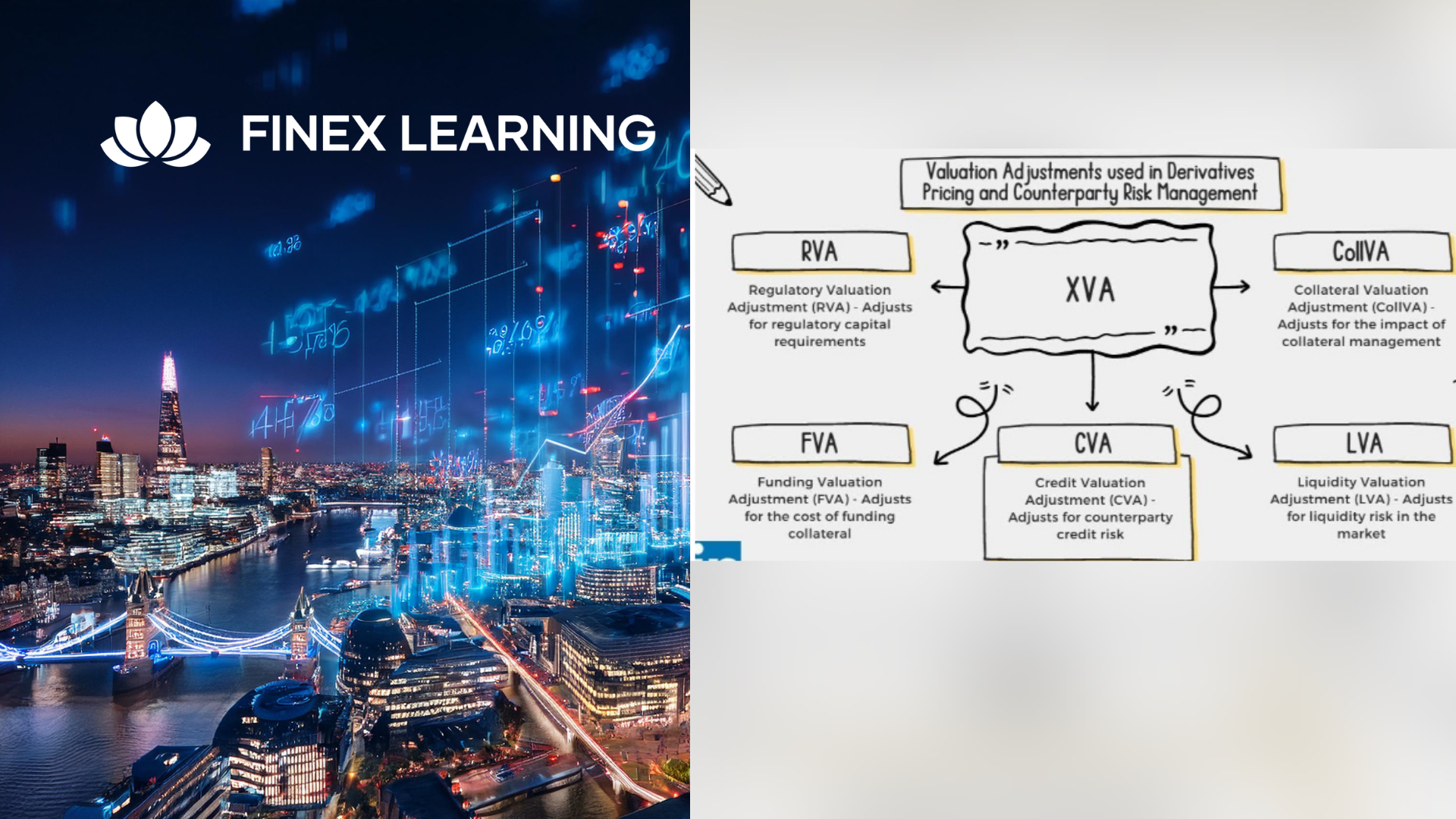

Learn how to calculate each XVA.

Learn sensitivities of each XVA and how XVA desks manage these.

Learn regulatory capital treatment of counterparty credit risk (both for CCR and CVA volatility) and how to stress test this within ICAAP or system-wide external, supervisor-led capital stress test.

Who the course is for

Anyone involved in OTC derivatives

XVA traders

XVA quants

Derivatives traders and salespeople

Risk management

Treasury staff

Internal audit and finance

Course Content

To learn more about the day by day course content please click here

To learn more about schedule, pricing & delivery options, book a meeting with a course specialist now