- Professional Development

- Medicine & Nursing

- Arts & Crafts

- Health & Wellbeing

- Personal Development

602 Courses in Nottingham

Overview 2 day course on scorecards, rating agency frameworks, regulation and integration and quantification of Environmental, Social and Governance (ESG) analysis into equity and credit investing / lending for / to corporates, banks and other financial institutions, applied to many case study companies and industries Who the course is for Investors and analysts – equity and credit; public and private Bank loan officers M&A advisors Restructuring advisors Course Content To learn more about the day by day course content please click here To learn more about schedule, pricing & delivery options, book a meeting with a course specialist now

Overview 2 day course on key interest rate derivative products, covering both theory (product mechanics, market conventions and valuation) and practice (wide range of applications for wide range of market participants showcased) Who the course is for Interest rate traders, salespeople and quants Asset-liability management staff with banks and insurance companies Fixed income and credit asset managers / hedge funds / pension funds / insurance companies Corporate treasurers Risk management Anyone using interest rate derivatives Course Content To learn more about the day by day course content please click here To learn more about schedule, pricing & delivery options, book a meeting with a course specialist now

Overview The objective of this course is to equip professionals with comprehensive knowledge and practical skills in WEB 3 technologies and crypto assets. Participants will gain a deep understanding of the underlying principles of blockchain, the operational mechanics of cryptocurrencies, the potential impact of these technologies on the banking sector and the latest trends. Who the course is for Consultants Analysts Managers C-Level executives People in need of knowledge to develop a blockchain strategy People working with blockchain projects Regulators Course Content To learn more about the day by day course content please click here To learn more about schedule, pricing & delivery options, book a meeting with a course specialist now

Overview 2 day applied course with comprehensive case studies covering both Standardized Approach (SA) and Internal Models Approach (IMA). This course is for anyone interested in understanding practical examples of how the sensitivities-based method is applied and how internal models for SES and DRC are built. Who the course is for Traders and heads of trading desks Market risk management and quant staff Regulators Capital management staff within ALM function Internal audit and finance staff Bank investors – shareholders and creditors Course Content To learn more about the day by day course content please click here To learn more about schedule, pricing & delivery options, book a meeting with a course specialist now

Overview This is a 2 day course to learn ALM tools to achieve strong and market-resilient, actuarially-resilient Solvency 2 (S2) ratios at Group consolidated level and at key cash-remitting entities to ensure dividend stability. For those not fully familiar with Solvency 2, this course is best taken in conjunction with “Solvency 2” Who the course is for Capital management / ALM / risk management staff within insurance company Investors in insurance company securities – equity, subordinated bonds, insurance-linked securities Salespeople covering insurance companies Course Content To learn more about the day by day course content please click here To learn more about schedule, pricing & delivery options, book a meeting with a course specialist now

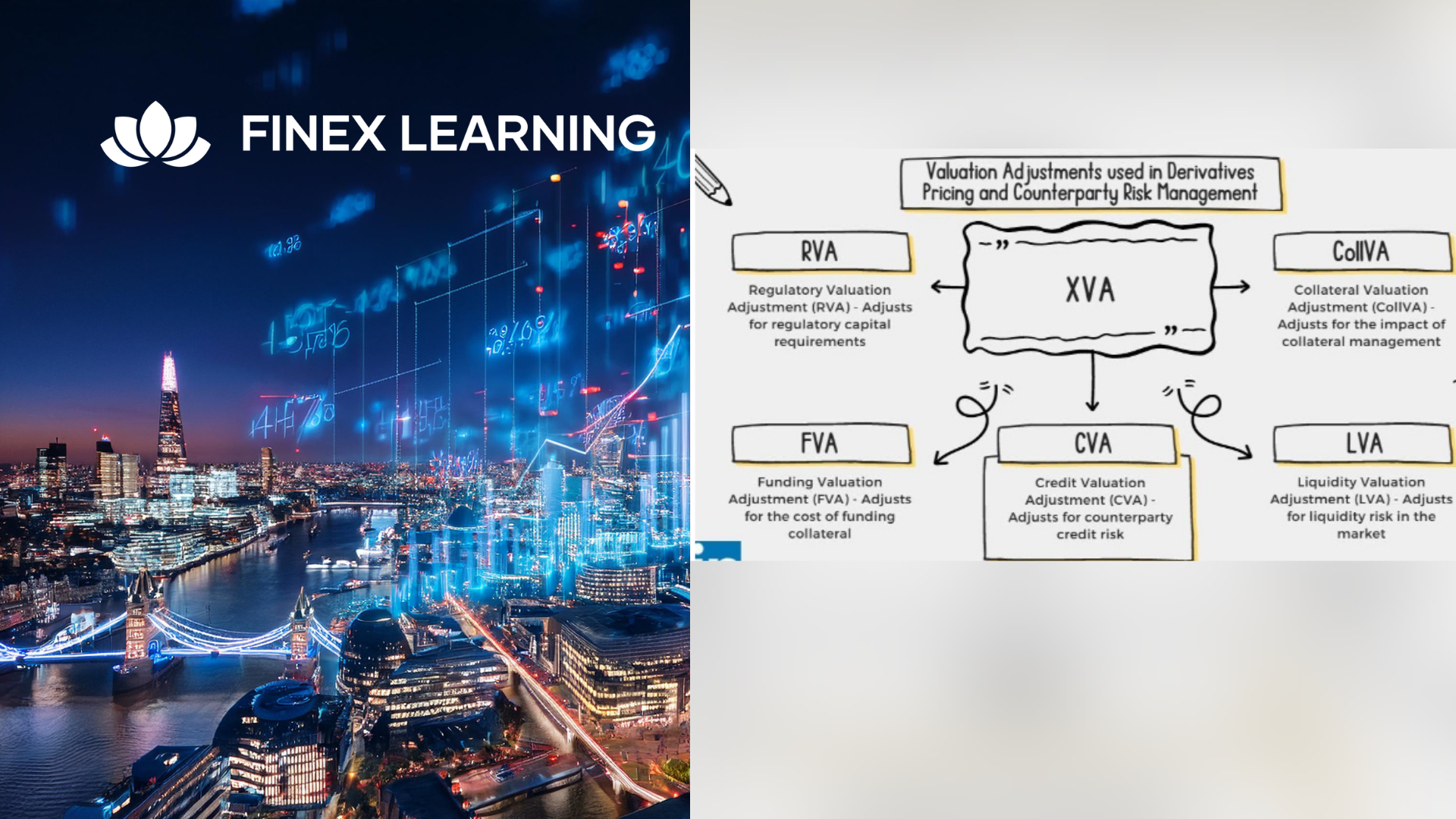

Overview This 1 day course focus on comprehensive review of the current state of the art in quantifying and pricing counterparty credit risk. Learn how to calculate each xVA through real-world, practical examples Understand essential metrics such as Expected Exposure (EE), Potential Future Exposure (PFE), and Expected Positive Exposure (EPE) Explore the ISDA Master Agreement, Credit Support Annexes (CSAs), and collateral management. Gain insights into hedging strategies for CVA. Gain a comprehensive understanding of other valuation adjustments such as Funding Valuation Adjustment (FVA), Capital Valuation Adjustment (KVA), and Margin Valuation Adjustment (MVA). Who the course is for Derivatives traders, structurers and salespeople xVA desks Treasury Regulatory capital and reporting Risk managers (market and credit) IT, product control and legal Quantitative researchers Portfolio managers Operations / Collateral management Consultants, software providers and other third parties Course Content To learn more about the day by day course content please click here To learn more about schedule, pricing & delivery options, book a meeting with a course specialist now

Overview A review of the most enduringly popular structured equity-linked products. This 1 day hands-on programme will help you gain familiarity with 1st generation & 2nd generation structured products convexity – and their applications. Discover techniques for maximising the participation rate to enhance returns for investors. Explore the trade-offs between coupon payments and gearing, and how they affect the risk-return profile of the notes. Explore ladder structures, their relationship to lookbacks, and the benefits they offer to investors. Learn about accumulators, their structuring, and the reasons behind their controversy in the market. Who the course is for Structured Products Desks, Financial Engineers, Product Controllers Traders, Dealing Room Staff and Sales People Risk Managers, Quantitative Analysts and Middle Office Managers Fund Managers, Investors, Senior Managers Researchers and Systems Developers Course Content To learn more about the day by day course content please click here To learn more about schedule, pricing & delivery options, book a meeting with a course specialist now

Overview This 2-day programme covers the latest techniques used for fixed income attribution. This hands-on course enables participants to get a practical working experience of fixed income attribution, from planning to implementation and analysis. After completing the course you will have developed the skills to: Understand how attribution works and the value it adds to the investment process Interpret attribution reports from commercial systems Assess the strengths and weaknesses of commercially available attribution software Make informed decisions about the build vs. buy decision Present results in terms accessible to all parts of the business Who the course is for Performance analysts Fund and portfolio managers Investment officers Fixed Income professionals (marketing/sales) Auditors and compliance Quants and IT developers Course Content To learn more about the day by day course content please click here To learn more about schedule, pricing & delivery options, book a meeting with a course specialist now

Overview This is a 2 day applied course on XVA for anyone interested in going beyond merely a conceptual understanding of XVA and wants practical examples of Monte Carlo simulation of market risk factors to create exposure distributions and profiles for derivatives used for XVA pricing Learn how to do Monte Carlo simulation of key market risk factors across major asset classes to create exposure distributions and profiles (with and without collateral) for derivatives used for XVA pricing. Learn how to calculate each XVA. Learn sensitivities of each XVA and how XVA desks manage these. Learn regulatory capital treatment of counterparty credit risk (both for CCR and CVA volatility) and how to stress test this within ICAAP or system-wide external, supervisor-led capital stress test. Who the course is for Anyone involved in OTC derivatives XVA traders XVA quants Derivatives traders and salespeople Risk management Treasury staff Internal audit and finance Course Content To learn more about the day by day course content please click here To learn more about schedule, pricing & delivery options, book a meeting with a course specialist now

Overview A 1-day course on inflation-linked bonds and derivatives, focusing on the UK market in particular. We examine how inflation is defined and quantified, the choice of index (RPI vs. CPI), and the most common cash flow structures for index-linked securities. We look in detail at Index-linked Gilts, distinguishing between the old-style and new-style quotation conventions, and how to calculate the implied breakeven rate. Corporate bond market in the UK, and in particular the role of LPI in driving pension fund activity. Inflation swaps and other derivatives, looking at the mechanics, applications and pricing of inflation swaps and caps/floors. The convexity adjustment for Y-o-Y swaps is derived intuitively. Who the course is for Front-office sales Product control Research Traders Risk managers Fund managers Project finance and structured finance practitioners Accountants, auditors, consultants Course Content To learn more about the day by day course content please click here To learn more about schedule, pricing & delivery options, book a meeting with a course specialist now